Picture supply: Getty Pictures

After spending a lifetime at work, all of us hope to benefit from the chill and benefit from the fruits of our labours. However precisely how a lot passive revenue will we have to dwell comfortably? This could differ considerably from individual to individual.

What is obvious, nonetheless, is that the quantity required for a superb way of life in retirement is rising steadily over time. It implies that making the suitable monetary selections when planning for later life is turning into more and more essential.

The excellent news is that traders at this time have extra alternatives than ever earlier than to hit their retirement objectives. Right here’s how I’m assured of attaining an opulent retirement.

The goal

As I discussed, the precise quantity an individual wants in later life will differ, relying on elements like their retirement objectives, the place they dwell, and their relationship standing.

But it’s price contemplating what the Pensions and Lifetime Financial savings Affiliation (PLSA) says the common particular person wants for a cushty retirement to get a tough ball park estimate.

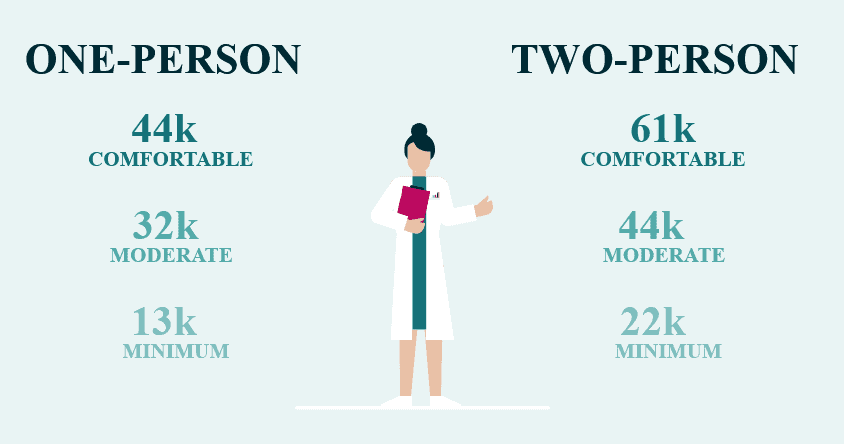

Its newest analysis reveals that the common one-person family requires a £43,900 yearly revenue for a cushty life-style. This degree of revenue would supply for necessities and extras like a a wholesome funds for meals and garments, a alternative automotive each three years, and a two-week vacation within the Med and frequent journeys away annually.

The determine for a two-person family is £60,600.

A £38k+ revenue

There are lots of paths people can take to hit that aim. They’ll put money into property, develop a facet hustle, or put cash in dividend- and capital gains-generating shares, as an example.

I’ve personally chosen to prioritise investing in world shares to make a retirement revenue, with some cash additionally put apart in money accounts to handle threat. With an 80-20 break up throughout these traces, I’m focusing on a mean annual return of at the very least 9% on my share investments and 4% on my money over the interval.

Let me present you ways this works. With a month-to-month funding of £400 in shares and money, I might — if all the pieces goes to plan — have a £641,362 nest egg to retire on.

If I then invested this in 6%-yielding dividend shares, I’d have an annual passive revenue of £38,482. Added to the State Pension (presently at £11,975), I might simply obtain what I’ll must retire in consolation.

Taking the US route

After all, investing in shares is riskier than placing all my cash in a easy financial savings account. Nonetheless, funds and trusts just like the iShares Core S&P 500 UCITS ETF (LSE:CSPX) can considerably scale back my threat whereas nonetheless letting me goal the robust long-term returns the US inventory market can present.

Keep in mind, although, that efficiency might be bumpy throughout broader share market downturns.

This exchange-traded fund (ETF) has holdings in all the companies listed on the S&P 500 index. In addition to offering me with wonderful diversification by sector and area, it offers me publicity to world-class firms with market-leading positions and powerful steadiness sheets (like Nvidia and Apple).

Since 2015, this iShares fund has supplied a mean annual return of 12.5%. If this continues, a daily funding right here might put me nicely on the right track for a wholesome passive revenue in retirement. It’s why I already maintain it in my portfolio.