If you happen to’re a TikTok person, you’ve most likely seen some movies about money stuffing, during which crisp greenback payments are counted and slid into smooth, labeled pouches. Whereas some viewers are drawn in merely for the aesthetic, others are impressed by the extremely sensible advantages of this type of budgeting.

Money stuffing isn’t a brand new idea, nevertheless it’s a classy time period for the age-old observe of envelope budgeting — which entails putting money into envelopes for every class in your price range, equivalent to housing, meals, transportation and utilities.

A profit of money stuffing is you’re much less prone to make impulse purchases when your cash is assigned a goal and tucked into labeled envelopes. Some discover it helps them reside inside their means, with out the stress of developing in need of payments or different bills every month.

Money stuffing doesn’t come with out main downsides, nonetheless. Merely put, cash within the financial institution is commonly safer, and the financial institution pays you curiosity. Fortuitously, nonetheless, you may observe “cashless money stuffing” to get the very best of each budgeting worlds.

Drawbacks of money stuffing

Two vital downsides of holding your cash at house in envelopes are:

- Your cash received’t earn curiosity.

- Funds won’t be recovered if misplaced or stolen.

You’re lacking out on curiosity

In the beginning, money stuffed into an envelope isn’t incomes any curiosity. Conversely, it’s not troublesome to discover a high-yield financial savings account that earns an annual proportion yield (APY) of 5 % or higher.

For instance, say you’re capable of commit $300 to financial savings each month. If you happen to deposit that quantity often right into a financial savings account that earns 5 % APY, in a single yr you’d have earned round $83 in curiosity. That’s $83 greater than you’d have by simply holding the money at house in an envelope.

Your cash’s safer within the financial institution

There could also be no strategy to get well money if it turns into misplaced or stolen from your house. Reasonably, it could be safer to maintain your cash in a federally insured checking account. This manner, your cash is protected if the monetary establishment fails, so long as your stability is inside the limits and pointers.

When banks carry this insurance coverage, it’s offered by means of the Federal Deposit Insurance coverage Corp. (FDIC). For credit score unions, this insurance coverage is thru the Nationwide Credit score Union Affiliation (NCUA). Having this insurance coverage means your deposit accounts are insured for as much as $250,000 per depositor, per insured financial institution or credit score union, for every account possession class.

“Holding money round the home means extra than simply lacking out on curiosity, however exposes you to the chance of loss or theft,” says Greg McBride, CFA, Bankrate chief monetary analyst. “Cash in a high-yield financial savings account with a financial institution or credit score union will earn curiosity but in addition be protected by federal deposit insurance coverage.”

Strategies of cashless money stuffing

Fortuitously, there are methods to categorize parts of your cash whereas nonetheless holding it protected and incomes curiosity. In different phrases, you may reap the advantages of money stuffing with out holding onto the money.

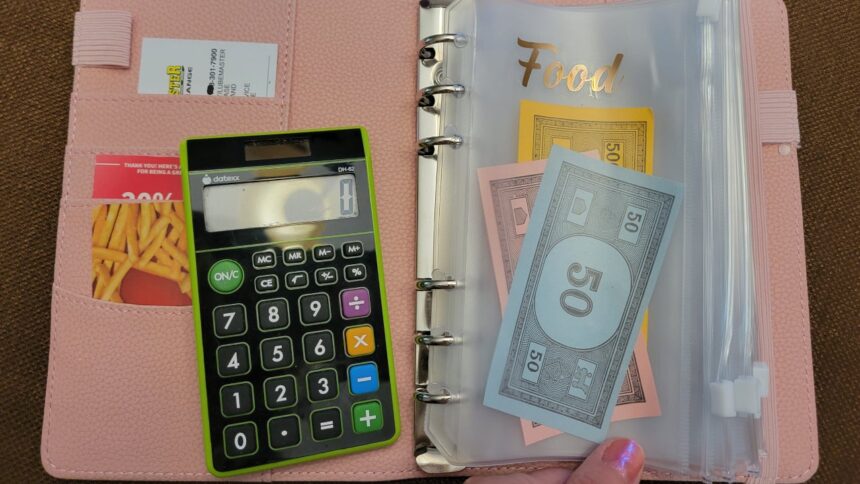

Use play cash

One strategy to categorize your cash with out holding money is to insert play cash — or any paper placeholder of your alternative — into envelopes. This lets you visualize how a lot you’re devoting to every of your month-to-month bills, whereas your actual cash is safely within the financial institution, incomes curiosity.

Each payday, insert placeholders into the envelopes as a substitute of actual cash, allocating the quantity you’ll want for mortgage or lease, meals, fuel and so forth. As cash is spent, take away the placeholders from the envelopes. When nothing is left in a given envelope, you’ve spent your allotted quantity for the month.

Use a budgeting app

You may incorporate the tried-and-true envelope budgeting technique with fashionable know-how by downloading a budgeting app that helps you categorize your spending. Some such apps even sync along with your financial institution accounts to conveniently present a full image of your spending and saving.

For instance, the GoodBudget app is predicated on the envelope budgeting technique. For every of your spending classes, cash can solely be taken from the corresponding envelope. Envelopes will also be devoted to financial savings classes, and the app permits a number of gadgets to sync to the account.

The PocketGuard app helps you to create customized spending classes, and it makes use of them to interrupt down how your cash is being spent. It additionally lets you know the way a lot spending cash you might have left all through the month.

Open an account with spending classes

Varied banks present their prospects with budgeting instruments, and a few of these could attraction to those that worth the envelope technique. For example, Ally Financial institution checking account holders can create as much as 30 spending buckets, permitting you to order cash within the account for upcoming bills. The app robotically subtracts cash from every bucket as you spend.

Equally, Huntington Financial institution checking account customers have varied in-app budgeting instruments. Clients can arrange spending classes, whereas establishing spending limits in addition to alerts on how a lot has been spent per class.

Backside line

The age-old technique of envelope budgeting gives varied cash administration advantages, nevertheless it comes with sure dangers. Through the use of actual envelopes and cash placeholders, a digital budgeting app or a checking account with spending classes, you may nonetheless profit from categorizing your spending whereas having fun with the security and interest-earning alternatives of cash within the financial institution.

![10 Creative Infographics & Why They Work [With Examples]](https://makefinancialcenter.com/wp-content/uploads/2025/10/image-for-guest-article-SEJ_1600x840_-1-150x150.png)